- Aeviva

- Posts

- These are top 5 BigPharma companies by Market Cap

These are top 5 BigPharma companies by Market Cap

Eli Lilly, Novo Nordisk, and three others are worth $2+ trillion combined - here's what they make, how they got so big, and why they dominate

In partnership with

Estimated Read Time: 6 minutes

Five pharmaceutical companies have a combined market value larger than the GDP of France.

Eli Lilly is worth more than Coca-Cola, Nike, and Netflix combined - thanks to one diabetes/weight-loss drug making $20+ billion annually.

These companies don't just make pills - they control the patents, research, and pricing for drugs treating billions of people worldwide.

Today's Issue

Main Topic: The top 5 pharmaceutical companies by market capitalization - what they make, why they're so valuable, and how they dominate global healthcare

Subtitles:

The rankings: top 5 pharma companies by market cap (2024)

#1: Eli Lilly - the Ozempic competitor worth $700+ billion

#2: Novo Nordisk - the GLP-1 king controlling weight-loss drugs

#3: Johnson & Johnson - the diversified giant that split in two

#4: Merck - the cancer immunotherapy powerhouse

#5: AbbVie - Humira's successor drugs and the biosimilar challenge

Abstract: The top 5 pharmaceutical companies by market capitalization (December 2024) are Eli Lilly ($720 billion), Novo Nordisk ($460 billion), Johnson & Johnson ($380 billion), Merck ($280 billion), and AbbVie ($310 billion), collectively worth $2.15 trillion driven primarily by GLP-1 weight-loss/diabetes drugs (Eli Lilly's Mounjaro/Zepbound generating $13.8 billion in 2024, Novo Nordisk's Ozempic/Wegovy generating $22 billion), cancer immunotherapy checkpoint inhibitors (Merck's Keytruda generating $25 billion annually becoming highest-revenue drug globally), and autoimmune biologics (AbbVie's Humira generating $20 billion before biosimilar competition, replaced by Skyrizi/Rinvoq generating $14 billion). Eli Lilly's valuation tripled 2022-2024 as Mounjaro (tirzepatide, dual GIP/GLP-1 agonist) demonstrated superior weight loss (22.5% body weight reduction vs 15% for Ozempic) creating $100+ billion addressable market for obesity treatment reaching 40% of US adults. Novo Nordisk dominates diabetes (controlling 50%+ global insulin market) and pioneered GLP-1 class with semaglutide (Ozempic/Wegovy) though manufacturing constraints limit supply. Johnson & Johnson spun off consumer health division Kenvue (2023) focusing on pharmaceuticals and medical devices, with key drugs including Darzalex (multiple myeloma, $9 billion), Stelara (autoimmune diseases, $10 billion), and Tremfya (psoriasis). Merck's dominance stems from Keytruda (pembrolizumab) treating 20+ cancer types with patent protection until 2028, while AbbVie transitions from Humira (lost US exclusivity 2023) to next-generation immunology drugs avoiding TNF-alpha mechanism facing biosimilar erosion.

The pharmaceutical industry concentrates enormous market value in relatively few companies because successful drug development requires decade-long timelines (10-15 years from discovery to approval), multi-billion dollar investments ($2-3 billion average per approved drug including failures), and patent-protected monopolies creating winner-take-all dynamics where breakthrough drugs generate $10-25 billion annually for 10-20 years before generic/biosimilar competition. The current top 5 pharmaceutical companies by market capitalization reflect several transformative healthcare trends: the explosive growth of GLP-1 receptor agonists (glucagon-like peptide-1 drugs) treating diabetes and obesity that expanded from $5 billion market in 2020 to projected $100+ billion by 2030 as drugs like Ozempic, Wegovy, Mounjaro, and Zepbound demonstrate 15-22% weight loss in clinical trials, the dominance of cancer immunotherapy particularly checkpoint inhibitors like Keytruda that unleash patients' immune systems against tumors generating unprecedented revenue for single drugs, and the maturation of biologic drugs (monoclonal antibodies and fusion proteins) treating autoimmune diseases that command premium pricing but face increasing biosimilar competition as patents expire. Understanding which companies dominate pharmaceutical markets requires examining their flagship products and patent timelines, why certain drug classes (GLP-1s, checkpoint inhibitors, TNF-alpha blockers) generate extraordinary revenue, how market valuations reflect pipeline strength and patent cliffs, and what strategic moves (spin-offs, acquisitions, R&D priorities) position these giants for future growth.

Lose Up to 23% Body Weight

MedVi’s GLP-1 treatments are clinically proven to help patients lose up to 23% of their body weight. Get personalized medical support, proven medications, and a plan designed to deliver real, lasting results.

Read all warnings before using GLP-ls. Side-effects may include a risk of thyroid c-cell tumors. Do not use GLP-1s if you or your family have a history of thyroid cancer. In certain situations, where clinically appropriate, a provider may prescribe compounded medication, which is prepared by a state-licensed sterile compounding pharmacy partner. Although compounded drugs are permitted to be prescribed under federal law, they are not FDA-approved and do not undergo FDA review for safety, effectiveness, or manufacturing quality.

#1: Eli Lilly - The Ozempic Competitor Worth $700+ Billion 🏆💊

Flagship drugs:

Mounjaro (tirzepatide for type 2 diabetes): Approved May 2022. Generated $5.8 billion in 2024, growing 300%+ year-over-year. Weekly injection demonstrating 12-22% weight loss in addition to blood sugar control.

Zepbound (tirzepatide for obesity): Approved November 2023. Generated $2.8 billion in first year. Same molecule as Mounjaro but marketed specifically for weight loss in patients without diabetes.

Trulicity (dulaglutide, older GLP-1): $7.4 billion annually, declining as patients switch to more effective Mounjaro.

Verzenio (breast cancer treatment): $4 billion annually, growing 20%+ as expanded indications approved.

Jardiance (diabetes SGLT2 inhibitor): $3.2 billion annually, also shows cardiovascular benefits.

*drug images are symbolic

Why Lilly is so valuable:

Superior efficacy: Mounjaro clinical trials showed 22.5% average weight loss (some patients lost 25%+) versus Ozempic's 15% weight loss. This superiority drove doctors and patients to preferentially choose Mounjaro despite being newer to market.

Dual mechanism: Tirzepatide activates both GLP-1 and GIP receptors (glucose-dependent insulinotropic polypeptide), while Ozempic only activates GLP-1. The dual action produces greater weight loss and blood sugar control.

Manufacturing capacity: Lilly invested $18+ billion in new manufacturing facilities (Indiana, North Carolina, Ireland, Germany) specifically for tirzepatide production, positioning to capture demand that Novo Nordisk cannot meet due to supply constraints.

Patent timeline: Mounjaro/Zepbound protected until 2040s, giving Lilly 15-20 years of exclusivity to dominate before biosimilars threaten.

Pipeline strength:

Orforglipron: Oral GLP-1 pill (currently injectable) showing 15% weight loss in Phase 2 trials. Could expand market to patients unwilling to inject weekly.

Retatrutide: Triple hormone agonist (GLP-1, GIP, glucagon) showing 24% weight loss in Phase 2 trials - potentially superior to Mounjaro.

Donanemab: Alzheimer's drug approved July 2024, though commercial success uncertain given modest efficacy and high cost.

💡 Fun Fact: Eli Lilly's market cap increase from 2022-2024 ($480 billion gain) equals the entire value of Coca-Cola Company. One drug class (GLP-1s) created half a trillion dollars in shareholder value in two years.

#2: Novo Nordisk - The GLP-1 King Controlling Weight-Loss Drugs 👑💉

Flagship drugs:

Ozempic (semaglutide for type 2 diabetes): Approved 2017. Generates $14 billion annually. Weekly injection became cultural phenomenon through social media and celebrity use despite being indicated only for diabetes.

Wegovy (semaglutide for obesity): Approved 2021. Generates $4.5 billion annually, constrained by manufacturing limits. Same molecule as Ozempic, higher dose, marketed specifically for weight loss.

Insulin portfolio: Tresiba (long-acting), Levemir, NovoLog (rapid-acting), NovoRapid generating $8 billion combined. Novo controls 50%+ of global insulin market.

Victoza/Saxenda (liraglutide, older GLP-1): $4 billion annually, declining as patients switch to more effective semaglutide.

Why Novo is so valuable:

Pioneered GLP-1 class: Novo developed first GLP-1 drugs (Victoza 2010, Ozempic 2017, Wegovy 2021), establishing brand dominance and clinical evidence base before competitors entered market.

Cardiovascular benefit: SELECT trial (2023) demonstrated Wegovy reduces cardiovascular events (heart attack, stroke) by 20% in obese patients, expanding insurance coverage beyond cosmetic weight loss to medical necessity.

Insulin monopoly: Controlling half the global insulin market provides steady $8 billion annual revenue base, diversifying beyond GLP-1 dependence.

Brand recognition: "Ozempic" became household name through aggressive marketing and social media virality, creating consumer demand that drives prescriptions.

The manufacturing crisis:

Novo cannot produce enough Ozempic/Wegovy to meet demand, creating 12-24 month waitlists at pharmacies. This supply constraint limits revenue growth and allows competitors (Lilly, Amgen, Pfizer) to capture market share.

Novo invested $6 billion expanding Danish and US manufacturing facilities, but new capacity won't come online until 2025-2026.

Patent timeline: Semaglutide protected until 2031-2033 depending on jurisdiction, giving Novo 7-9 years remaining exclusivity before biosimilars threaten.

Pipeline:

CagriSema: Combination of semaglutide and cagrilintide (amylin agonist) showing 25% weight loss in Phase 2 trials - potentially superior to Mounjaro.

Once-monthly GLP-1: Icodec showing similar efficacy with monthly dosing, improving convenience.

💡 Critical Context: Novo's manufacturing constraints are both blessing and curse. Limited supply maintains high prices and prevents market saturation, but allows Eli Lilly to capture explosive growth Novo cannot access. If Novo solved manufacturing, revenue could double, but margins might compress from competition.

#3: Johnson & Johnson - The Diversified Giant That Split in Two 🏥🔬

Flagship pharmaceutical drugs:

Darzalex (daratumumab for multiple myeloma): $9.5 billion annually, growing 20%+. Monoclonal antibody targeting CD38 on cancer cells. Combination with chemotherapy became standard care.

Stelara (ustekinumab for Crohn's disease, ulcerative colitis, psoriasis): $10 billion in 2023, declining as biosimilars launch following patent expiration. IL-12/IL-23 inhibitor, once J&J's top drug.

Tremfya (guselkumab for psoriasis, psoriatic arthritis): $3.5 billion annually, growing 30%+. IL-23 inhibitor replacing Stelara as it loses exclusivity.

Imbruvica (ibrutinib for blood cancers): $4 billion annually (split with AbbVie partnership). BTK inhibitor for chronic lymphocytic leukemia and lymphomas.

Erleada (apalutamide for prostate cancer): $2.2 billion annually, growing 25%+.

Strengths:

Diversification reduces risk: Unlike Merck (40%+ revenue from Keytruda) or AbbVie (formerly 50%+ from Humira), J&J spreads revenue across 10+ drugs and medical devices, protecting against patent cliffs.

Strong oncology pipeline: Multiple cancer drugs in development, positioning for continued growth as Darzalex eventually faces biosimilar competition.

Decades of operational excellence: J&J consistently ranks among most admired companies, with strong R&D productivity and commercial execution.

Challenges:

Multiple patent cliffs: Stelara lost exclusivity 2023, Imbruvica faces generic competition 2026-2027, Darzalex protected until 2030s. Replacing $15+ billion in declining revenue requires pipeline success.

Limited obesity exposure: No GLP-1 drugs in portfolio, missing explosive growth category driving Lilly and Novo valuations.

Talc litigation overhang: Thousands of lawsuits alleging baby powder caused cancer, with billions in potential liabilities creating investor uncertainty.

#4: Merck - The Cancer Immunotherapy Powerhouse 🎯🔬

Flagship drug - Keytruda dominance:

Keytruda (pembrolizumab) generates $25 billion annually, making it the highest-revenue pharmaceutical drug globally. Checkpoint inhibitor blocking PD-1 receptor, approved for 20+ cancer types including melanoma, non-small cell lung cancer, head and neck cancer, Hodgkin lymphoma, bladder cancer, kidney cancer, gastric cancer, cervical cancer, liver cancer, esophageal cancer.

Why Keytruda dominates:

First-mover advantage: Approved 2014 as first PD-1 inhibitor, accumulating years more clinical data than competitors (Opdivo, Tecentriq, Libtayo), making doctors comfortable prescribing it.

Combination therapies: Keytruda combined with chemotherapy shows superior efficacy versus chemotherapy alone, making it standard first-line treatment for many cancers.

Earlier-stage expansion: Originally approved for metastatic (late-stage) cancer, now approved for earlier-stage disease and adjuvant therapy (after surgery to prevent recurrence), expanding patient population.

Other significant drugs:

Gardasil/Gardasil 9 (HPV vaccine): $9.5 billion annually. Prevents cervical cancer, throat cancer, genital warts caused by human papillomavirus. Growing in emerging markets.

Januvia/Janumet (diabetes DPP-4 inhibitors): $4 billion annually, declining as GLP-1s prove superior.

Lynparza (ovarian/breast cancer PARP inhibitor): Partnership with AstraZeneca, $2.5 billion Merck share.

Pipeline strategy:

Merck investing heavily in Keytruda combinations (with chemotherapy, with other immunotherapies, with targeted therapies) and earlier-stage cancer vaccines to extend Keytruda franchise beyond 2028. Success uncertain.

💡 Pro Tip: Merck's valuation entirely depends on whether pipeline drugs can replace Keytruda's $25 billion. Current pipeline shows no single drug capable of this, meaning Merck likely shrinks post-2028 unless multiple drugs combine to fill gap.

#5: AbbVie - Humira's Successor Drugs and the Biosimilar Challenge 💊📉

The Humira story:

Humira (adalimumab) was the highest-revenue drug in pharmaceutical history, generating $20+ billion annually at peak (2018-2022). TNF-alpha blocker treating rheumatoid arthritis, Crohn's disease, ulcerative colitis, psoriasis, ankylosing spondylitis.

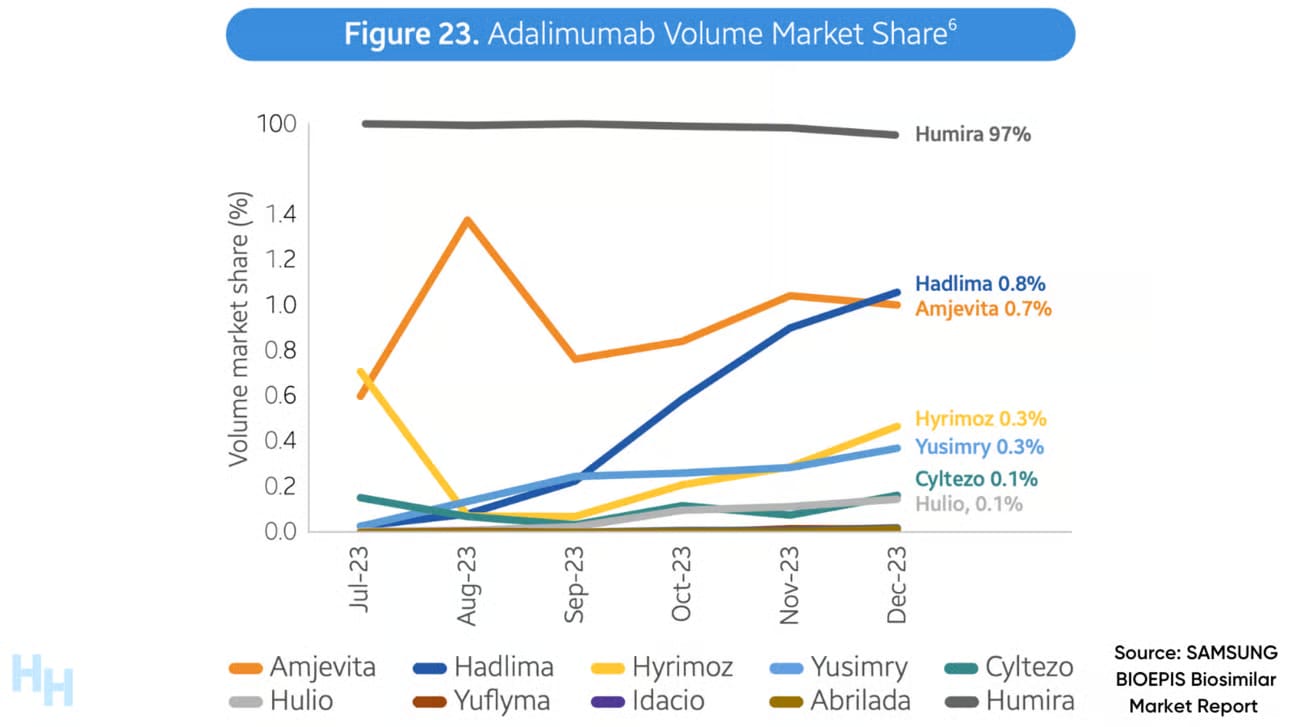

Humira Biosimilars

Lost US patent exclusivity January 2023, triggering biosimilar competition from Amjevita, Hadlima, Cyltezo, Hyrimoz, Yuflyma, Abrilada (6+ competitors).

Humira revenue collapsed from $21 billion (2022) to $8 billion (2024) as biosimilars captured 60%+ market share through 30-50% discounts.

International revenue declining similarly as European patents expire.

The succession strategy:

AbbVie spent decade developing next-generation immunology drugs using different mechanisms to avoid biosimilar competition:

Skyrizi (risankizumab, IL-23 inhibitor): $7.8 billion in 2024, growing 50%+ annually. Treats psoriasis, psoriatic arthritis, Crohn's disease. Superior efficacy to Humira in head-to-head trials, dosed every 12 weeks versus Humira's every 2 weeks, improving patient compliance.

Rinvoq (upadacitinib, JAK inhibitor): $4.4 billion in 2024, growing 60%+ annually. Treats rheumatoid arthritis, psoriatic arthritis, ulcerative colitis, atopic dermatitis. Oral pill versus Humira's injection, appealing to needle-averse patients. FDA added black box warnings for blood clots and infections, slowing but not stopping growth.

The transition challenge:

AbbVie must replace Humira's $20+ billion peak revenue with Skyrizi/Rinvoq growth. Current trajectory suggests $15+ billion combined by 2027, partially filling gap. However, total company revenue declining 2023-2025 during transition, creating investor uncertainty.

Other drugs providing diversification:

Imbruvica (blood cancer): Partnership with J&J, $4 billion AbbVie share, declining as newer BTK inhibitors launch.

Botox (medical and cosmetic): $5 billion annually. Treats chronic migraines, overactive bladder, muscle spasticity, plus cosmetic wrinkles. Stable revenue, minimal competition.

Venclexta (blood cancer BCL-2 inhibitor): $3 billion annually, growing.

💡 Critical Context: AbbVie's entire business model depended on one drug (Humira) for 15 years. The company essentially bet its future on two successor drugs working. So far, the gamble appears paying off, but safety concerns (Rinvoq black box warnings) and competition (Eli Lilly developing oral IL-23 inhibitors) create ongoing risks.

The Proven System Fitness Instructors Use to Grow Online

Discover Kajabi’s 30 Days to Launch: Scale Your Fitness Business Online guide. Launch online programs, memberships, and digital products while keeping in-person clients. Step-by-step roadmap, success stories, and AI prompts included.

Takeaways

Top 5 pharmaceutical companies (Eli Lilly $720B, Novo Nordisk $460B, Johnson & Johnson $380B, AbbVie $310B, Merck $280B) collectively worth $2.15 trillion, with rankings dominated by GLP-1 weight-loss/diabetes drugs (Lilly's Mounjaro/Zepbound $13.8B, Novo's Ozempic/Wegovy $22B) and cancer immunotherapy (Merck's Keytruda $25B becoming highest-revenue drug globally).

Eli Lilly's valuation tripled 2022-2024 as Mounjaro demonstrated superior 22.5% weight loss versus Ozempic's 15%, capturing explosive $100+ billion obesity treatment market reaching 40% of US adults, while Novo Nordisk faces manufacturing constraints limiting ability to meet demand despite pioneering GLP-1 class and controlling 50%+ global insulin market.

Traditional pharma giants face patent cliffs and strategic transitions: Johnson & Johnson spun off consumer division Kenvue (2023) focusing on pharmaceuticals/devices, Merck depends on Keytruda for 40%+ revenue (patent expires 2028), AbbVie replacing Humira ($20B peak, now $8B with biosimilars) with next-generation Skyrizi/Rinvoq ($14B growing 50-60% annually) requiring successful pipeline execution maintaining market dominance.

Feedback & Sponsorship

What'd you think of this week's newsletter? Hit reply to let us know. Did we crush it? Blow your mind? We read every response.

Want your brand in front of hundreds of thousands of readers? Contact us for sponsorship opportunities [email protected]

Want more where that came from? Head to our website

Feeling Anxious? You are not alone

Get help from a licensed therapist - anytime, anywhere. BetterHelp has helped over 5 million people, with no commitment, 100% online.

Take the first step, with 25% off your first month, and a network of 30,000 therapists to choose from. BetterHelp therapy is HSA + FSA eligible. Just take our quiz to get matched with a therapist and start your journey.

This email was delivered by a third-party, on behalf of BetterHelp. Copyright © 2025 BetterHelp. All Rights Reserved. 990 Villa St, Mountain View, California, United States.

Reply